What if the biggest barrier to your Mediterranean lifestyle isn't the property price, but the 30% difference in how Spanish banks treat international buyers? You've likely spent hours browsing coastal homes, only to feel a wave of anxiety when researching mortgages in spain for non residents. It's natural to worry about language barriers or hidden fees that might complicate your journey toward a life in the sun.

We've designed this guide to help you master the financing process with absolute clarity, ensuring you understand how to secure the 60% to 70% LTV typical for international investors in 2026. As your local experts, we're here to provide the professional expertise and personal warmth needed for a secure transaction. Discover a clear checklist of required documents, an overview of borrowing limits, and a roadmap to getting a fair market rate so you can focus on your new dream home.

Key Takeaways

- Understand the financial benchmarks for 2026, including the 60-70% LTV rule and how the 35% debt-to-income ratio impacts your borrowing power.

- Navigate the evolving landscape of mortgages in spain for non residents by comparing the benefits of fixed, variable, and the increasingly popular mixed-rate options.

- Simplify your application process by learning the essential steps to secure your NIE and open the right Spanish bank account for your investment needs.

- Explore how a dedicated partner can bridge the gap between you and English-speaking lenders to ensure a smooth, transparent, and secure property purchase.

Understanding Mortgages in Spain for Non-Residents

Start your journey to Mediterranean living by mastering the financial landscape of the Costa del Sol and beyond. A non-resident mortgage is a specialized loan designed for individuals who pay their primary income taxes outside of Spain. As we move through 2026, the Spanish property market has reached a level of maturity that offers unique stability for international buyers. Understanding Mortgages in Spain is the first step toward securing your dream home in the sun while protecting your financial interests with a "trygg affär" approach.

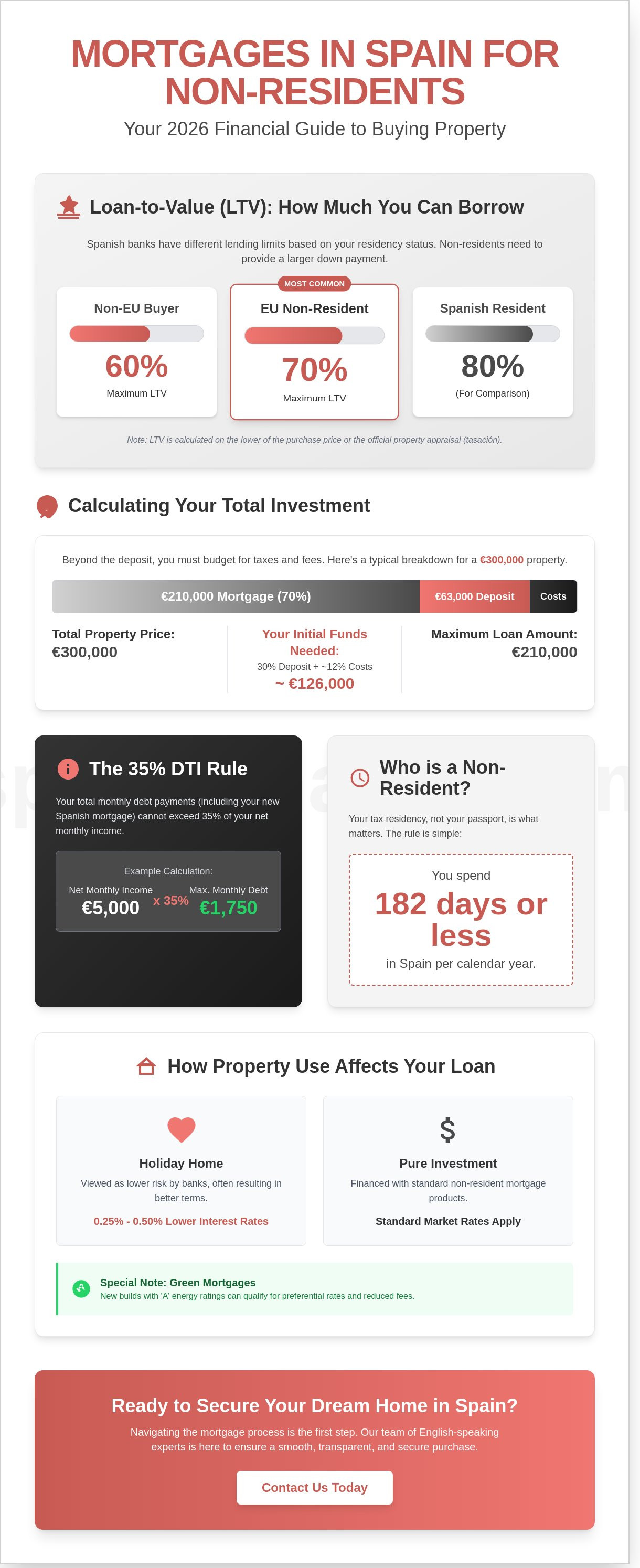

Spanish banks apply different criteria depending on your tax status. While residents often access higher leverage, mortgages in spain for non residents typically offer a Loan-to-Value (LTV) ratio capped between 60% and 70%. This conservative lending environment acts as a safeguard, ensuring you maintain healthy equity from day one. Using a Spanish mortgage also functions as a natural currency hedge. By matching your debt to the asset's currency, you shield yourself from the volatility of exchange rates. If you choose to rent out your property, your Euro-denominated rental income directly covers your Euro mortgage payments, removing the stress of fluctuating conversion costs.

Who Qualifies as a Non-Resident Buyer?

Residency isn't determined by your nationality but by where you spend your time and pay your taxes. The 183-day rule is the definitive metric. If you spend 182 days or fewer in Spain during a calendar year, you're classified as a non-resident. In 2026, lenders prioritize the stability of your income source over your passport. EU citizens often benefit from streamlined digital paperwork, but non-EU applicants from countries like the UK, USA, or Norway are highly valued. You'll simply need to provide a more comprehensive dossier of your fiscal solvency from your home country to satisfy modern compliance standards.

The Purpose of the Loan: Holiday Home vs. Investment

Lenders categorize your loan based on how you intend to use the property, which directly impacts your offer. A holiday home for personal use is often viewed as a lower risk. Banks recognize the emotional attachment to a second home, which historically leads to lower default rates. Consequently, these loans often feature interest rates that are 0.25% to 0.50% lower than pure investment products. In 2026, new build villas are attracting the most competitive financing terms. Because these properties meet the latest "A" rated energy efficiency standards, many Spanish banks now offer "Green Mortgages" with reduced setup fees and preferential margins to encourage sustainable investment.

Key Financial Requirements: LTV and Eligibility

Securing your dream home under the Mediterranean sun requires a clear understanding of the Spanish banking landscape. For those seeking mortgages in spain for non residents, lenders prioritize stability and liquidity over speculative growth. You'll find that Spanish banks are welcoming, yet they adhere to strict risk assessments to ensure a trygg affär, or safe deal, for both parties. In 2026, the baseline for eligibility remains a combination of a solid down payment and a transparent financial history.

Spanish lenders generally apply a 35% debt-to-income ratio. This means your total monthly debt obligations, including your existing mortgage at home and the new Spanish loan, shouldn't exceed 35% of your net monthly income. If you earn a net salary of €5,000, your total global debt payments must stay below €1,750. Banks also look for a minimum property purchase price, often starting at €100,000, with minimum loan amounts typically set at €50,000.

Loan-to-Value (LTV) Limits for Non-Residents

While Spanish residents can often access 80% financing, non-residents are currently capped at 70% LTV. If you're a buyer from outside the EU, some banks might even limit this to 60%. This percentage is calculated based on the lower of two values: the agreed purchase price or the official appraisal value, known as the tasación. If a property is priced at €300,000 but the appraiser values it at €280,000, your 70% loan will be based on the €280,000 figure.

- The Deposit: Expect to provide 30% of the property price from your own funds.

- Buying Costs: You must budget an additional 12% to 15% on top of the deposit to cover ITP (Transfer Tax), notary fees, and land registry costs.

- Liquidity: Banks prefer seeing these funds already available in a liquid account.

Discover how we can simplify this process by visiting our guide on finding your Spanish home with confidence.

Income and Currency Considerations

The Mortgage Credit Directive, specifically Article 28 of the Spanish Mortgage Law, significantly influences how you borrow if you earn in SEK, NOK, or GBP. This legislation allows borrowers to convert their mortgage into their local currency under specific conditions. To mitigate the resulting exchange rate risk, many Spanish banks have become more selective with non-Euro earners. They often apply a "haircut" to your foreign income, sometimes counting only 80% of your salary toward the affordability calculation to buffer against currency fluctuations.

Preparation is your best tool. You'll need to provide three to six months of bank statements, your latest tax returns, and a credit report from your home country. Providing a clear, well-organized financial profile helps the bank see you as a low-risk partner, moving you one step closer to your life in the sun.

Interest Rate Options in 2026: Fixed, Variable, or Mixed?

Finding the right financing is the bridge between your current life and your future home in the sun. In 2026, the landscape for mortgages in spain for non residents has evolved to favor flexibility and security. While the European Central Bank's policies have stabilized after years of transition, the Spanish market now emphasizes "Mixed" mortgage products. These hybrids offer a fixed rate for the initial 3, 5, or 10 years, followed by a variable rate tied to the Euribor. This structure protects your budget during the crucial early years of ownership while allowing you to benefit from potential rate drops later in the loan's life.

Fixed rates remain the gold standard for investors seeking long-term peace of mind. By locking in a rate, you insulate yourself from global economic shifts and interest rate hikes. In 2026, fixed rates for non-residents typically sit between 3.4% and 4.1%, depending on your loan-to-value ratio. Variable rates are strictly for the risk-tolerant. With the Euribor projected to hover around 2.75% throughout 2026, your monthly payments will fluctuate annually. However, the rise of "Green Mortgages" offers a modern financial advantage. If you choose an energy-efficient new build with an A or B rating, many lenders now provide a "green discount" of up to 0.20% on your interest spread, rewarding your commitment to a sustainable Mediterranean lifestyle.

Choosing the Right Rate Structure

Fixed rates act as a shield against future inflation, ensuring your holiday home costs remain predictable for decades. If you prefer a middle ground, mixed rates are the 2026 market favorite. You'll typically enjoy a lower fixed rate for the first 5 years before the loan transitions to a variable structure. Don't worry about being trapped; Spanish law in 2026 continues to cap early repayment penalties. For fixed loans, the maximum penalty is generally 2% during the first 10 years, dropping to 1.5% thereafter, giving you the freedom to clear your debt early as your circumstances change.

Hidden Costs and Mortgage Clauses

Opening fees, known as comisión de apertura, are a standard part of mortgages in spain for non residents, but they shouldn't be a surprise. In the current market, a fee of 0.5% to 1% is considered fair and standard. You'll also encounter "linked products" like life and home insurance. While banks often offer interest rate discounts if you use their providers, you aren't legally required to accept them. Your Notary plays a vital role here. By law, you must meet with them at least 24 hours before the signing. They'll walk you through every clause to ensure you feel confident, secure, and fully informed before you step into your new life in Spain.

Step-by-Step Application Process and Documentation

Securing mortgages in spain for non residents requires a structured approach that balances administrative precision with local knowledge. Your journey begins with the NIE (Número de Identidad de Extranjero). This tax identification number is mandatory for every financial transaction in Spain, from signing a utility contract to buying a villa. You can apply for this at a Spanish consulate in your home country or via a representative with power of attorney in Spain. Once you have your NIE, opening a Spanish bank account is your next move. While digital banking has advanced significantly by 2026, many traditional lenders still prefer an in-person meeting to finalize the account setup and verify your identity.

After your initial application, the bank will issue two vital documents: the FEIN (European Standardised Information Sheet) and the FiAE (Standardised Addendum Sheet). These aren't just brochures; they are formal, binding offers that detail every interest rate, fee, and condition of your loan. In Spain, transparency is legally mandated. You'll enter a mandatory 10-day cooling-off period (14 days in Catalonia) after receiving these documents. You cannot sign the mortgage before this period ends. This law ensures you have ample time to review the terms without pressure, creating a sense of security during a major life decision.

The Essential Document Checklist

Banks need to see a clear picture of your financial health. Prepare these documents in advance to avoid delays in the approval process:

- Proof of income: Your last three payslips and your most recent tax return (P60 or equivalent).

- Bank statements: Six months of records showing your salary deposits and everyday spending habits.

- Credit reports: An official report from agencies like Experian or TransUnion to prove your reliability.

- Property documents: A Nota Simple from the Land Registry and the signed purchase contract (Arras).

Timeline: From Application to Completion

In 2026, the average processing time for non-resident loans is approximately six to eight weeks. Applying for mortgages in spain for non residents is a manageable process when you have the right team by your side. Once the bank approves your profile and the property valuation (tasación) is complete, the file moves to the Gestoría. These administrative professionals handle the tax payments and registry filings. The final stage happens at the Notary's office. You, or your representative, will meet the bank's representative to sign the mortgage deed. Expect the Notary to read the entire document aloud to ensure you understand your obligations before the keys to your dream home are handed over.

Securing Your Spanish Home with Spaindinavia’s Support

Finding mortgages in spain for non residents can feel like a maze, but you don't have to walk it alone. Spaindinavia acts as your bridge to the Spanish financial system. We connect you with trusted English-speaking banks that understand the 2026 lending climate. This removes the language barrier and ensures you understand every clause of your offer before committing. Our team provides personalized guidance from your first viewing until the moment you hold the keys in your hand.

We manage the complex triangle between your solicitor, the bank, and the developer. By synchronizing these three parties, we prevent the delays that often derail property closings. For instance, we ensure the bank's appraiser has access to the site exactly when needed. This keeps the timeline on track for your move-in date. Our focus on New Build Villas simplifies the mortgage process significantly. Banks in 2026 often offer more favorable Loan-to-Value (LTV) ratios for new constructions because the property valuations are transparent and the energy efficiency ratings meet the highest EU standards. This makes your application much more attractive to lenders.

Our Network of Independent Experts

We work exclusively with independent solicitors who specialize in international law. These experts verify every document and certificate before you sign anything. Through our long-standing agency partnerships, we often access "off-market" mortgage conditions. These are specific interest rates or flexible terms not advertised to the general public. We prioritize security and transparency, ensuring you see every fee and tax upfront so there are no surprises at the notary. You get the best of both worlds: local Spanish expertise and a Scandinavian commitment to clarity.

Start Your Journey Today

Your journey to the Mediterranean coast begins with a viewing of our hand-picked portfolio of properties. We prioritize a "trygg affär" (secure deal), a core Swedish concept that ensures every aspect of your purchase is handled with the highest integrity. We aren't just selling houses; we're helping you build a new lifestyle under the sun. From the initial search to the final signature, we're your partner on the ground. Let us help you find your dream home and the right financing so you can start enjoying the Spanish life you've always imagined.

Your Path to a Mediterranean Lifestyle Starts Here

Navigating the market for mortgages in spain for non residents requires a clear strategy and the right local partners. In 2026, lenders typically offer non-residents a 70% loan-to-value ratio, making it essential to have your capital and documentation organized early. Choosing between fixed and mixed interest rates will define your long-term financial comfort. Spaindinavia has specialized in new build villas since 2016, acting as a reliable bridge between your aspirations and the Spanish property market. We've established deep partnerships with leading English-speaking Spanish banks to ensure you receive clear, transparent advice. Our experts provide comprehensive support through every milestone, from obtaining your NIE to the final appointment at the Notary. We're here to ensure a secure deal that lets you focus on the excitement of your new home. You're not just buying a property; you're investing in a higher quality of life under the sun. Let's begin this journey together with confidence and warmth.

Explore New Build Villas and Secure Your Financing with Spaindinavia

Frequently Asked Questions

Can I get a mortgage in Spain if I am retired?

Yes, you can secure a mortgage in Spain as a retiree if you demonstrate a stable pension income. Spanish lenders typically require your pension to cover the monthly repayments while maintaining a debt-to-income ratio below 35 percent. You'll need to provide your last 3 months of pension statements and your most recent tax return. Many retirees successfully fund their dream home this way, provided the loan term concludes before they reach the bank's age limit.

What is the maximum age for a non-resident mortgage in Spain?

Most Spanish banks set the maximum age for mortgage completion at 75 years old. This means if you're 60 today, your mortgage term can't exceed 15 years. Some specific lenders like Sabadell or Santander might extend this to 80 if you have a guarantor or additional collateral. Always calculate your term based on the oldest applicant's age to ensure your application meets these strict criteria. It's a vital step in planning your long-term investment.

Do I need to be in Spain in person to apply for a mortgage?

You don't need to be physically present in Spain to apply for or even sign your mortgage. By granting a Power of Attorney to a trusted lawyer, they can handle the entire process on your behalf. This legal document must be signed before a notary, either in Spain or at a Spanish consulate in your home country. It's a common practice that saves you multiple international flights during the 6 to 8 week approval period.

How much are the closing costs for a property with a mortgage in Spain?

Closing costs for a property with a mortgage in Spain typically range between 10 percent and 15 percent of the purchase price. These costs include the Property Transfer Tax, which varies by region like 10 percent in Valencia or 7 percent in Andalusia. You'll also pay notary fees, land registry fees, and a mandatory bank appraisal. Since the 2019 Mortgage Law, banks now cover the AJD tax and most administrative costs, reducing the burden on the buyer.

Can I get a mortgage in Spain as a self-employed non-resident?

Yes, self-employed individuals can obtain mortgages in Spain for non residents by providing comprehensive financial records. Lenders usually demand 2 years of audited accounts and tax returns to verify your income stability. You should also prepare a letter from your accountant confirming your business's health. While the paperwork is more intensive, banks regularly approve these loans if your net income comfortably covers the 30 percent to 35 percent debt-to-income threshold. It's about showing consistency in your earnings.

Is it better to get a mortgage in Spain or in my home country?

Getting a mortgage in Spain is often better because it eliminates currency exchange risks if your property is the collateral. Spanish banks offer competitive rates specifically for the local market, often with fixed terms that provide long-term security. If you borrow in your home country, you might face higher interest rates or struggle to find a lender willing to secure a loan against a foreign asset. It's simpler to keep the debt where the property sits.

What happens if the bank appraisal is lower than the purchase price?

If the bank appraisal comes in lower than the purchase price, the bank will calculate your loan amount based on that lower valuation. For example, if you buy for 300,000 Euro but the appraisal is 280,000 Euro, a 70 percent mortgage will only cover 196,000 Euro. You'll need to cover the remaining 104,000 Euro from your own savings. This scenario occurs in roughly 15 percent of transactions in fast-moving markets, so having a cash buffer is essential for a smooth purchase.

How long is a mortgage offer (FEIN) valid for in Spain?

A binding mortgage offer, known as the FEIN, is typically valid for 30 days once issued by the bank. Under Spanish law, you must wait a mandatory 10 day cooling off period after receiving this document before you can sign the deed at the notary. This ensures you have ample time to review the terms without pressure. If you don't sign within the 30 day window, you might need to restart the application or request a formal extension from the lender.