What if the biggest hurdle to your Mediterranean dream isn't the property price, but how you structure your cash before you even step inside? It's a common worry. You've found a stunning new build villa or a cozy resale apartment, but the math behind the scenes feels like a moving target. You likely find yourself asking, "how much deposit do i need for a spanish property" while trying to distinguish between mortgage down payments and legal reservation fees. It's natural to feel a bit of hesitation when non-refundable payments are on the line and tax percentages seem to vary by region.

We understand that clarity is the foundation of a safe deal. In this 2026 guide, you'll discover the exact breakdown of the 30% to 40% deposit typically required by Spanish banks for non-residents, alongside the 8% to 13% needed for taxes and closing costs. We'll walk you through the entire financial timeline, from the initial 10% Arras agreement to the final notary appointment. By the end, you'll have a clear, percentage-based roadmap to ensure your investment is handled safely and professionally, letting you focus on the joy of your new life in the sun.

Key Takeaways

- Calculate the total liquid cash required for 2026, typically 30% to 40% for non-residents, to understand exactly how much deposit do i need for a spanish property.

- Navigate the legal nuances of the Arras agreement, the standard 10% deposit that secures your home and formalizes the seller's commitment.

- Factor in the essential 10-15% buffer for taxes and closing costs, including IVA for new builds and ITP for resale properties.

- Identify the differences in payment timelines between staged payments for new build villas and the more immediate requirements of resale apartments.

- Discover how expert legal vetting and the Spaindinavia approach provide a secure bridge to your new life in the sun.

The Total Cash Required: How Much Deposit Do I Need for a Spanish Property?

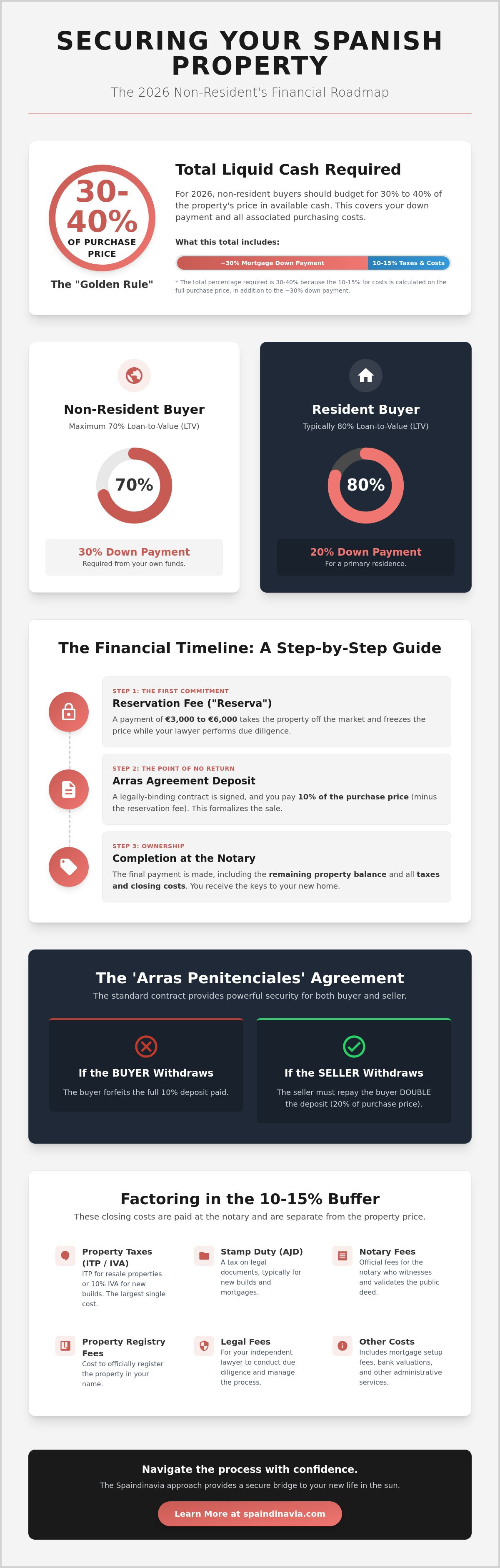

Planning your budget for a home in the sun starts with one essential figure: the total cash you have in the bank. For 2026, the "Golden Rule" is to budget for 30% to 40% of the purchase price in liquid cash. This ensures you can cover the gap between the bank's mortgage offer and the actual price of the home. Understanding exactly how much deposit do i need for a spanish property is the first step toward a secure purchase, as it prevents any last minute surprises at the notary's office.

You must distinguish between the "purchase deposit" paid to the seller and the "mortgage down payment" required by your bank. While they both come from your savings, they serve different legal purposes. The total deposit you need is the sum of the mortgage gap plus approximately 12% for closing costs.

Resident vs. Non-Resident Requirements

Your residency status is the biggest factor in determining your loan-to-value (LTV) ratio. Spanish residents typically secure 80% LTV mortgages for their primary residence, meaning they only need to provide a 20% down payment. Non-residents usually need a 30% deposit because Spanish banks currently offer a 70% LTV maximum for second homes or international buyers. In May 2026, banks have implemented tighter internal risk rules, moving away from broad pricing and toward offers tied strictly to your financial profile.

Learning from the Spanish property market history, modern lenders are far more cautious. With the Euribor sitting near 2.25% in early 2026, banks are prioritizing stability. They often require non-residents to show more significant liquidity to offset higher funding costs. If you are looking at properties above €500,000, be aware that some banks have removed full fixed-rate options, making these loans primarily variable or mixed-rate products.

The Minimum Entry Point: Reservation Fees

The very first payment you will make is the "Reserva" or reservation fee. This isn't the full deposit yet, but it's the most critical step to secure your dream home. Once paid, the reservation fee removes the property from the market and freezes the price while your lawyer performs due diligence. Typical reservation amounts range from €3,000 to €6,000. We always recommend having this amount ready in a reachable account, as the best resale apartments and new build villas often move quickly. This fee is later deducted from the total purchase price, acting as your initial commitment to the transaction.

Understanding the Arras Agreement: The Legal Deposit

Once you've secured your chosen home with a reservation fee, you'll move toward the most significant legal milestone: the Arras contract. This document is widely considered the "point of no return" in a Spanish property transaction. It's a private agreement between you and the seller that sets the final terms of the sale and establishes a firm deadline for completion at the Notary. While the initial reservation fee was a small gesture of intent, the Arras payment is a serious financial commitment.

People often ask, "how much deposit do i need for a spanish property" during this phase, and the answer is almost universally 10% of the total purchase price. This amount is standard across Spain for resale apartments, townhouses, and villas alike. When you sign this contract, you'll pay the 10% (minus the reservation fee already paid), and this sum is held as a guarantee. On the day of completion, this entire amount is deducted from the final balance you pay to the seller.

Types of Arras Contracts in Spain

Not all contracts are created equal. The most common type for residential sales is the Arras Penitenciales. We prefer this version because it offers the highest level of security and "trygghet" for our clients. It provides a clear exit strategy for both parties, albeit with a cost. If you decide to back out of the deal after signing, you will lose your 10% deposit. However, if the seller decides to withdraw, the law requires them to pay you back double the amount you deposited. This "double-your-money" rule acts as a powerful deterrent against sellers who might try to accept a higher offer from another buyer at the last minute.

You might occasionally hear about Arras Confirmatorias. These are less common for private buyers because they don't allow for a simple penalty-based exit. Instead, they imply a binding obligation where either party can legally force the other to fulfill the contract through the courts. For most people looking for a stress-free purchase, the Penitenciales route is the standard choice.

Protecting Your Legal Deposit

Protecting your money requires more than just a signature. You must work with an independent solicitor to review every line of the Arras agreement before you transfer any funds. One of the most critical protections to include is a "subject to mortgage" clause. In the current 2026 lending climate, where banks have stricter internal risk rules, this clause ensures that if your mortgage application is rejected, you can recover your deposit. Without this specific wording, you could lose your entire 10% if your financing falls through.

Your solicitor will also perform essential checks to ensure the property is free of debts and that the seller is the rightful owner. If you want to ensure your journey is handled with this level of care, you can speak with our local experts to find the right legal partners. We believe that a safe transaction is the only way to truly enjoy your new life in the sun.

Deposit Structures: New Build Villas vs. Resale Properties

The path to your dream home looks different depending on whether you choose a modern, key-ready new build or a charming resale property. While the total answer to "how much deposit do i need for a spanish property" remains centered around that 30% to 40% threshold for non-residents, the timing of these payments varies significantly. New build villas offer a gradual financial journey, whereas resale apartments require a more immediate concentration of capital.

For those choosing new construction, your money is protected by a legal requirement called an Aval Bancario. This is a bank guarantee that ensures every cent you pay during the construction phase is secured. If the developer fails to complete the project, this guarantee ensures your funds are returned with interest. We always verify that these guarantees are in place because your peace of mind is our priority.

The New Build Payment Timeline

Buying a new build villa or bungalow allows you to spread your costs over the duration of the construction, which often takes 12 to 24 months. This staged approach is helpful for managing liquidity. The process typically follows three distinct steps:

- Stage 1: Reservation fee. You pay an average of €6,000 to take the property off the market and lock in the current price.

- Stage 2: Private Purchase Contract (PPC). Within 30 to 60 days, you usually pay between 20% and 30% of the purchase price, minus the reservation fee already paid.

- Stage 3: Completion. The remaining 60% to 70% is paid at the Notary once the building is finished and the Licencia de Primera Ocupación (First Occupation License) is issued.

Managing currency exchange is vital during these staged payments. If you are transferring funds from a non-euro account, fluctuations over 18 months can significantly alter your final cost. We suggest using a specialist currency broker to lock in rates, ensuring your budget stays predictable.

The Resale Payment Timeline

Resale properties follow a much faster, two-step deposit process. There is less flexibility here, so you must have your liquid cash ready before you begin your search. Once you find the right home, the timeline moves quickly to ensure a smooth transition of ownership.

- Initial Reservation. Similar to new builds, a small fee reserves the home while your lawyer conducts searches.

- The Arras Agreement. As discussed previously, you will pay the full 10% legal deposit within 14 to 30 days of the reservation.

- Escritura Pública. The final balance, including all taxes and the mortgage contribution, is paid at the signing of the public deed, usually 6 to 8 weeks after the initial reservation.

Resale purchases offer less time to organize financing, but they allow you to move in and start enjoying the Mediterranean lifestyle almost immediately. Whether you prefer the staged payments of a new villa or the speed of a resale apartment, we ensure every step is handled with professional care and personal warmth.

Factoring in the 12%: Taxes and Closing Costs

When calculating how much deposit do i need for a spanish property, many buyers make the mistake of only looking at the down payment for the mortgage. To secure your home with absolute confidence, you must budget for an additional 10% to 15% on top of the purchase price. These funds cover the mandatory taxes and administrative fees that formalize your ownership. Think of this as the final layer of your investment that transforms a property into your legal home and ensures your "trygg affär" (safe deal) is complete.

The specific tax you pay depends entirely on the type of property you choose. For resale apartments, townhouses, or bungalows, you pay the Property Transfer Tax, known as ITP (Impuesto de Transmisiones Patrimoniales). This rate varies by autonomous community but generally sits between 7% and 10% of the purchase price. It's a one-time payment made after the completion at the notary. For a full list of expenses, see our Buying Property in Spain Guide: The Essential 2026 Checklist.

VAT (IVA) and Stamp Duty on New Homes

New build villas attract a different tax structure that requires careful planning. You'll pay 10% Value Added Tax (IVA) across most of mainland Spain, though this drops to 7% if you're buying in the Canary Islands. Additionally, you must factor in Stamp Duty, known as AJD (Actos Jurídicos Documentados). In 2026, AJD typically hovers around 1.5% depending on the region where the property is located. It's vital to remember that these taxes are usually paid at the final signing at the Notary. They don't form part of your initial 10% Arras deposit, so you need to keep this liquidity separate and ready for the completion date.

Legal and Administrative Fees

Professional guidance is your best insurance policy during this transition. A solicitor is a non-negotiable cost, typically charging around 1% of the property price plus VAT for their services. They handle the complex legal checks that ensure your investment is safe and that no hidden debts follow the property. Notary and Land Registry fees are fixed by law based on the property value and the complexity of the deeds. These usually range from €1,000 to €2,500 for a standard residential home.

Finally, don't forget minor banking fees. Spanish banks often charge for issuing the "banker's drafts" or OMF transfers required for the final payment on completion day. These small administrative details are what we help you manage to ensure a stress-free experience. Ready to see the numbers for your specific dream home? Contact our team for a personalized cost breakdown.

Securing Your Investment: The Spaindinavia Approach

Buying a home abroad is more than just a financial transaction; it's a significant life decision that deserves a partner who understands your perspective. We act as a bridge between Scandinavian expectations of efficiency and the unique nuances of the Spanish property market. While you now have a clearer picture of how much deposit do i need for a spanish property, our role is to ensure that every euro you commit is protected by rigorous legal standards and local expertise.

We believe that security is the foundation of inspiration. This is why we collaborate exclusively with independent solicitors who vet every Arras contract before a single transfer is made. For those investing in new build villas or townhouses, we ensure that mandatory bank guarantees are issued for every staged payment. This level of oversight removes the fear of non-refundable payments and provides you with the "trygg affär" (safe deal) that our clients have come to expect from us.

Our support extends far beyond the property search. We provide personalized assistance to help you navigate the administrative landscape, from opening your Spanish bank account to obtaining your NIE (tax identification number). These practical steps are often where confusion arises, but with our team by your side, the process remains calm and well-structured. We're here to make sure you feel at home even before you receive the keys.

Transparency in the Buying Process

Trust is built on clarity. We operate with a policy of absolute transparency, meaning there are no hidden markups or surprise fees in our service. Our commission-based model is straightforward, allowing us to focus entirely on finding the right fit for your lifestyle. Every client receives a step-by-step financial roadmap that aligns with the 2026 market conditions we've discussed. To understand the long-term potential of your purchase, you can explore how to maximize your returns in our Spain Property Investment Guide.

Next Steps: From Deposit to Dream Home

The journey to your life in the sun begins with a single, confident step. We invite you to browse our hand-picked portfolio of quality villas, bungalows, and resale apartments along the coast. Once you find a property that speaks to your heart, we can provide a detailed "Cost of Purchase" simulation. This document breaks down the specific deposit, taxes, and fees for that exact home, so you know exactly how much deposit do i need for a spanish property before you even book a viewing flight.

Let us help you turn the uncertainty of percentages and legal terms into the excitement of a new beginning. Contact our team today for a stress-free transition to your Mediterranean dream home.

Take the Next Step Toward Your Spanish Home

Understanding the financial landscape is the first step toward a secure investment in the sun. You now know that answering "how much deposit do i need for a spanish property" involves budgeting for a 30% to 40% cash reserve to cover both the mortgage gap and approximately 12% in mandatory closing costs. Whether you choose the staged payment structure of a new build villa or the faster timeline of a resale apartment, legal protection through a vetted Arras contract is your greatest asset.

Since 2016, we've been specialists in the Costa Cálida and Costa Blanca regions, acting as a trusted partner for those seeking a "trygg affär" (safe deal). Our hand-picked portfolio is supported by independent solicitors and established banks to ensure every staged payment is protected by a bank guarantee. We take pride in handling the technical complexities and administrative hurdles so you can focus on the joy of your new Mediterranean lifestyle.

Start your secure property journey with Spaindinavia today and let us guide you home. Your dream of a life in the sun is within reach, and we're ready to help you make it a reality.

Frequently Asked Questions

Is the property deposit refundable if I change my mind?

Property deposits are generally not refundable if you simply change your mind after signing an Arras Penitenciales contract. Under Spanish law, if you withdraw from the deal, the seller keeps the full 10% deposit as compensation. However, if the seller backs out, they're legally required to pay you back double the amount you deposited. This system provides a balanced level of security for both parties during the transaction.

Can I pay the deposit with a credit card or cash?

You can typically pay the initial reservation fee of €3,000 to €6,000 using a credit card to secure the property quickly. However, the larger 10% Arras deposit must be paid via bank transfer to comply with Spanish anti-money laundering regulations. Cash payments for property transactions are strictly limited by law, so a transparent bank-to-bank transfer is always the safest and most professional method for your records.

Does the 10% Arras deposit count towards my mortgage down payment?

Yes, the 10% Arras deposit counts directly toward your total purchase price and your mortgage down payment. For example, if you're a non-resident asking how much deposit do i need for a spanish property and the bank requires 30%, your 10% Arras payment covers the first third of that requirement. You would then provide the remaining 20% from your liquid savings at the notary on completion day.

What happens to my deposit if the bank rejects my mortgage application?

Your deposit is only protected if your solicitor has included a specific "subject to mortgage" clause in the Arras agreement. In the 2026 lending environment, where banks have stricter internal risk rules, this clause is vital for your peace of mind. Without it, failing to secure financing is considered a breach of contract, and you'd likely lose the full 10% deposit already paid to the seller.

Are new build deposits safe if the developer goes bankrupt?

New build deposits are highly secure because developers are legally required to provide an Aval Bancario or insurance policy for all staged payments. This bank guarantee ensures that if the developer fails to complete the project, your funds are returned to you with legal interest. We always verify these guarantees are active before our clients transfer any funds for new build villas or townhouses.

Do I need to pay the deposit from a Spanish bank account?

While you can often pay the initial 10% deposit from an international account, you'll eventually need a Spanish bank account for the final completion. Most notaries and sellers prefer "bankers drafts" issued by a local bank for the final balance payment. Additionally, having a local account is necessary for setting up your utility bills and paying your ongoing property taxes once you've moved in.

How much extra should I budget for non-resident property taxes?

You should budget between 8% and 13% on top of the purchase price to cover non-resident taxes and closing costs. This includes 10% IVA for new build properties or between 7% and 10% ITP for resale apartments, depending on the specific region. Adding roughly 1% for legal fees and another 1% for notary and land registry costs ensures you have a complete and safe financial roadmap.

What is the typical timeframe between paying the deposit and moving in?

The timeframe depends on the property type you choose. For a resale apartment, the process from paying the 10% deposit to receiving the keys usually takes between 4 and 8 weeks. If you're purchasing a new build villa off-plan, the timeline typically extends to 12 or 24 months, allowing you to manage your staged payments as the construction progresses toward the final notary signing.