Successful Spanish home ownership in 2026 isn't just about the deposit; it requires a triple-pot savings strategy that covers the purchase, the transition, and the first year of maintenance. It's natural to feel a flutter of anxiety when considering the 11% ITP tax in Valencia or how currency fluctuations might shift your budget overnight. We know that finding your place in the sun is a deeply personal journey, and we're here to ensure that journey feels calm and well-organised from the very first day.

This saving for a second home in spain checklist provides the comprehensive financial roadmap you need to navigate the current market with total confidence. We'll help you set a precise savings target, understand why banks now require a 30% to 40% down payment, and prepare for the 12-month Euribor rates currently sitting between 2.0% and 2.4%. You'll gain a clear, month-by-month planning guide that secures your investment and protects you from hidden costs whilst your property is vacant, allowing you to focus on the life-changing joy of Mediterranean living.

Key Takeaways

- Define the "Total Cost of Ownership" mindset to ensure your budget covers everything from regional taxes to the first year of property maintenance.

- Master the triple-pot strategy using our saving for a second home in spain checklist to effectively manage your deposit, transaction fees, and transition funds.

- Navigate the 2026 mortgage market with clarity on non-resident loan-to-value ratios and how current Euribor rates impact your monthly borrowing costs.

- Create a stress-free transition by following a chronological 12-month roadmap for administrative essentials like your NIE and opening a Spanish bank account.

- Learn why partnering with an independent solicitor is the most effective way to protect your capital and ensure a secure, transparent property investment.

Understanding the True Cost: Why Your Savings Goal Matters

Your journey towards a Mediterranean lifestyle begins long before you step onto a sun-drenched terrace in the Costa Blanca. Whilst it's tempting to browse listings and fall in love with a specific price tag, the sticker price is merely the starting point. Successful buyers in 2026 adopt a "Total Cost of Ownership" mindset, ensuring their saving for a second home in spain checklist accounts for the hidden layers of property acquisition. Beyond the deposit, you'll need to budget for taxes, legal fees, and the initial costs of making the house a home. Planning for these extras early prevents the stress of last-minute financial hurdles.

Defining Your Property Goals

Choosing between a sleek new build apartment and a charming resale villa significantly alters your financial roadmap. New build properties attract a national VAT (IVA) rate of 10%, plus a regional Stamp Duty (AJD) which stands at 1.4% in the Valencia region as of June 2026. Conversely, resale properties are subject to Property Transfer Tax (ITP). In Andalusia, this is a flat 7%, but if you're looking at the Costa Blanca, expect to pay 9% for properties under €1 million and 11% for those above. Deciding on your property type early allows you to pin down these percentages with precision.

The 2026 Market Outlook for Second Home Buyers

The Spanish real estate market has shown remarkable resilience and maturity when viewed through the lens of the Economic History of Spain. In early 2026, we're seeing a stabilised environment where mortgage interest rates for non-residents have settled between 3.0% and 3.8%. However, banks remain cautious, typically requiring a down payment of 30% to 40% of the property's appraised value. There's also a legislative backdrop to consider; a draft bill from May 2025 proposed a 100% purchase tax for non-EU residents. Whilst this isn't law, it highlights why staying informed and organised is vital for securing your investment.

Starting your financial organisation 12 months before your planned purchase is the gold standard for a reason. This window gives you ample time to audit your current assets, monitor currency exchange trends, and settle into a consistent savings rhythm. It also allows you to secure your NIE (tax identification number) and open a Spanish bank account without feeling rushed. By the time you're ready to sign the "Escritura", your saving for a second home in spain checklist will be a source of confidence rather than a cause for concern. We've seen that the most relaxed buyers are always the ones who did the maths a year in advance.

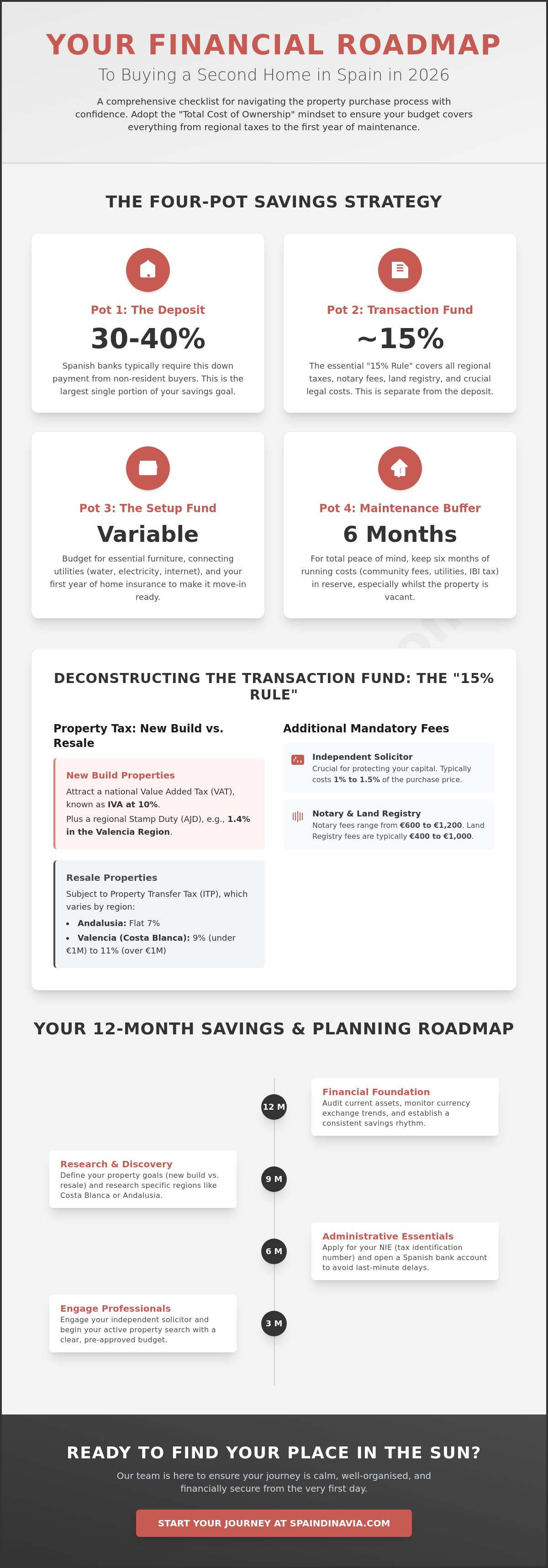

The Saving for a Second Home in Spain Checklist: Your Financial Pots

Organising your capital into four distinct "pots" is the most effective way to ensure your dream move remains a joyous experience. A comprehensive saving for a second home in spain checklist isn't just about the purchase price. It's about the security of knowing every eventuality is covered. We suggest categorising your funds into the following pillars to maintain total control over your investment.

- Pot 1: The Deposit: Spanish banks typically require a down payment of 30% to 40% of the purchase price for non-residents.

- Pot 2: The Transaction Fund: Use the "15% Rule" to cover regional taxes, notary fees, and legal costs.

- Pot 3: The Setup Fund: This covers essential furniture, utility connections, and initial home insurance.

- Pot 4: The Maintenance Buffer: Keep six months of running costs in reserve for total peace of mind whilst the property is vacant.

Breaking Down the 15% Taxes and Fees Rule

The "15% Rule" is a vital benchmark for your Transaction Fund. This pot covers the essential legalities and taxes that vary by region. For example, in the Valencia region, the ITP tax for resale properties is 9% for homes under €1 million, whilst new builds attract a 10% IVA plus 1.4% AJD. You should also budget between €600 and €1,200 for notary fees and roughly €400 to €1,000 for Land Registry fees. Engaging an independent solicitor usually costs between 1% and 1.5% of the purchase price. Following the UK Government Guide to Buying Property in Spain will help you cross-reference these legal requirements with your own checklist. Don't forget small but necessary allocations for your NIE application and Spanish bank account setup fees.

The Furnishing and Snagging Budget

The Setup Fund is where many buyers find themselves short. If you're purchasing a new build villa or apartment, it often arrives as a blank canvas. This means you must account for white goods, furniture, and potentially air conditioning installations. We also strongly advise saving for a professional snagging report for new properties. This ensures any minor construction flaws are identified and rectified by the developer before you take possession. Finally, your Maintenance Buffer should hold at least six months of running costs. This includes IBI (municipal tax), community fees, and utility standing charges. It ensures your investment remains secure even when you aren't there to enjoy the sun. If you're beginning to map out your budget, our team can help you identify investment properties that align with your financial goals.

By compartmentalising your savings this way, you avoid the anxiety of unexpected bills. You'll move into your new home knowing that the financial foundation is as solid as the property itself. This structured approach is what separates a stressful purchase from a successful lifestyle investment.

Financing Strategies: Mortgages vs. Cash Savings

Deciding between a cash purchase and a Spanish mortgage is one of the most significant choices on your saving for a second home in spain checklist. Whilst cash offers simplicity and speed, current financing options in 2026 provide a strategic opportunity to keep your capital liquid for other investments. Both paths require a clear understanding of the Spanish banking system's unique requirements for non-resident buyers, especially as lenders have become more selective with their criteria.

Spanish Mortgages for Non-Residents

Spanish lenders have maintained a steady appetite for non-resident borrowers throughout early 2026, though they prioritise stability. You can typically expect a maximum Loan-to-Value (LTV) ratio of 60% to 70% of the property's appraised value. This means your initial savings must cover the remaining 30% to 40% plus the transaction fees mentioned in our previous sections. Fixed interest rates currently range from 3.0% to 3.8%, whilst variable options track the 12-month Euribor, which sits between 2.0% and 2.4% as of May 2026. Banks will scrutinise your debt-to-income ratio, usually capping it at 35% to 40% of your net monthly income. If you own a primary residence in the UK, releasing equity can be a viable alternative to a Spanish mortgage, though this requires careful consideration of interest rate differences between the two countries.

Managing the GBP to EUR Exchange Rate Risk

For British buyers, the volatility of the GBP to EUR exchange rate is often the most overlooked financial risk. A seemingly small shift of 2% in the rate can add thousands of pounds to your final purchase price overnight. We recommend using a forward contract to protect your budget. This financial tool allows you to lock in a specific exchange rate for up to 12 months, ensuring your saving for a second home in spain checklist remains accurate regardless of market fluctuations. By fixing your rate early, you eliminate the gamble and gain the certainty needed to commit to a property with confidence. Additionally, providing a higher deposit than the bank's minimum can often secure you a more competitive interest rate, significantly reducing your long-term borrowing costs and protecting your Mediterranean lifestyle for years to come. Taking these steps ensures your investment is as secure as the sun is bright on the Costa Blanca.

The 12-Month Savings Roadmap: A Chronological Checklist

The most common mistake buyers make is falling in love with a property before their finances are ready to support the dream. A chronological approach ensures you aren't just saving money, but also preparing the administrative foundation required for a smooth transaction. This saving for a second home in spain checklist breaks your journey into manageable phases, allowing you to move forward with certainty and poise.

Phase 1: Foundation and Goal Setting (Months 12-9)

Your first trimester is dedicated to an honest audit of your current assets. Review your monthly income and expenses to determine a sustainable savings rate that won't compromise your lifestyle. This is the time to set your "Triple Pot" target, accounting for the 30% to 40% deposit and the 15% transaction fund we discussed earlier. By establishing these figures now, you give yourself a concrete goal to work towards. You should also check your credit score in your home country, as Spanish banks will review this during your mortgage application process.

Phase 2: Administrative Readiness (Months 8-6)

Once your savings rhythm is established, focus on the Spanish paperwork that often causes delays. Applying for your NIE (tax identification number) can take several weeks or even months depending on the consulate's workload. Simultaneously, research and open a Spanish bank account. Having this in place early allows you to transfer small amounts of capital over time, potentially taking advantage of favourable exchange rates. It also demonstrates to sellers that you're a serious, prepared buyer when the time comes to make an offer.

Phase 3: Execution and Property Viewing (Months 5-1)

As you enter the final five months, consult with a currency specialist to discuss the forward contracts mentioned in the previous section. You should also seek mortgage pre-approval from a Spanish lender. Knowing you qualify for a 25-year term with an LTV of 60% to 70% clarifies your exact purchasing power. In the final two months, finalise your emergency buffer and begin your property search in earnest. You're now in a position of strength, ready to act quickly when the right home appears. Discover our latest new build villas to see how your savings goal translates into a real Mediterranean home.

Following this timeline prevents the frantic rush that often leads to financial oversights. You've organised your pots, secured your administrative footing, and protected your capital against market shifts. Now, the only thing left to do is find the keys to your new life in the sun.

Protecting Your Savings: Ensuring a Secure Investment

You've diligently followed your saving for a second home in spain checklist, and now your capital is ready. Protecting that hard-earned money is the final, most critical step in your journey. We believe that a secure investment is built on transparency and expert legal oversight. This is where an independent solicitor becomes your most valuable ally. They don't just process paperwork; they act as a shield, verifying that the property is free of historical debts and that all construction permits are fully compliant with local urbanistic laws. Before you sign any contracts, reading our comprehensive buying property in Spain guide is the next logical step to ensure your investment is watertight.

Maximising ROI through Rental Management

Many of our clients choose to integrate a rental management strategy to help their property pay for itself. By listing your home as a holiday rental property, you can offset annual running costs like the IBI and community fees. It's vital to account for Non-Resident Income Tax (IRNR) in your calculations. As of May 2026, the tax rate is 19% for EU residents and 24% for non-EU residents on imputed income. Professional management ensures your home is cared for whilst you're away, preventing the small maintenance issues that can turn into expensive repairs if left unchecked. It's a proactive way to safeguard the funds you've worked so hard to accumulate.

Why a Hand-Picked Portfolio Saves You Money

At Spaindinavia, we focus on helping you avoid "money pits" by only presenting properties that meet our rigorous standards for quality and location. We look beyond the aesthetic appeal to assess the long-term Spain property investment potential of every villa or apartment. This means focusing on areas with high demand and low hidden maintenance risks. Our approach is designed to give you the same sense of security you feel in your primary home.

- We vet developers for new build projects to ensure financial stability and proven track records.

- We check the structural integrity of resale properties to avoid unforeseen renovation costs.

- We prioritise properties with high energy efficiency ratings to reduce future utility bills and increase resale value.

Your dream of a life in the sun deserves a foundation of absolute security. By combining a disciplined saving for a second home in spain checklist with expert local guidance, you can step into the Spanish market with total peace of mind. We're here to guide you through every financial and legal nuance, ensuring your transition to the Mediterranean is as smooth as possible. Let us help you find a secure investment today and turn your financial roadmap into a reality.

Take the First Step Towards Your Mediterranean Future

Securing your dream home in the sun is a journey that rewards the well-prepared. By masterfully managing your triple-pot strategy and following a disciplined saving for a second home in spain checklist, you've already laid the groundwork for a successful investment. You now understand that navigating the 2026 market requires more than just a deposit; it demands a clear roadmap covering regional taxes, currency fluctuations, and long-term maintenance buffers. This structured approach ensures your transition is defined by excitement rather than uncertainty.

With over 10 years of experience in the Spanish property market, we're dedicated to making your purchase as seamless as possible. We collaborate closely with independent legal and financial experts to ensure every transaction is watertight and transparent. Whether you're searching for high-yield new build villas or a charming resale apartment, our hand-picked portfolio is designed to protect your capital and your lifestyle. Start your secure Spanish property journey with Spaindinavia today and let us help you find the perfect place to call home. The warmth of the Costa Blanca is waiting for you.

Frequently Asked Questions

How much deposit do I need for a second home in Spain in 2026?

Non-resident buyers typically need a deposit of 30% to 40% of the property's appraised value. Spanish banks in early 2026 are conservative with their Loan-to-Value (LTV) ratios, usually capping lending at 60% to 70% for those living outside of Spain. It's essential to include this target on your saving for a second home in spain checklist early. Remember that this deposit must be liquid and ready before you sign the "Arras" deposit contract to avoid missing out on preferred listings.

What are the hidden costs of buying property in Spain?

The primary hidden costs are regional taxes and administrative fees, which usually add 12% to 15% to the purchase price. In the Valencia region, you'll encounter a 9% ITP tax for resales or 10% VAT for new builds. You must also budget €600 to €1,200 for notary fees and roughly 1% of the price for independent legal advice. These costs are often overlooked by first-time buyers but are vital for a secure transaction.

Can I get a mortgage in Spain as a British resident?

Yes, British residents can readily access Spanish mortgages, though the terms differ from those offered to residents. In early 2026, lenders offer non-residents fixed rates between 3.0% and 3.8% for terms up to 25 years. Banks will require proof of income and a debt-to-income ratio below 40%. It's helpful to get a pre-approval letter from a Spanish bank before starting your property search to confirm your exact budget and borrowing power.

Is it better to buy a new build or a resale property for a second home?

Choosing between a new build and a resale property depends on your budget for taxes and immediate maintenance. New builds attract 10% VAT but offer superior energy efficiency and a ten-year structural guarantee. Resale properties are subject to ITP tax, which is 7% in Andalusia, and often require an immediate "setup fund" for renovations or modernisation. New builds are often favoured by those seeking high-yield holiday rental properties with minimal initial repairs.

How much should I budget for monthly maintenance in Spain?

You should budget approximately €150 to €300 per month for basic maintenance of a standard apartment, excluding mortgage payments. This covers the IBI municipal tax, community fees, home insurance, and utility standing charges. For a villa with a private pool and garden, these costs can rise to €400 or more per month. Keeping a six-month maintenance buffer in your savings ensures your property remains secure whilst it's vacant and protects you from unexpected repairs.

Do I need a Spanish bank account before I start saving?

You don't need a Spanish bank account to start your initial savings, but you'll need one at least six months before your purchase. Having an account in Spain allows you to transfer funds gradually and cover administrative costs like the NIE application. It also simplifies the process of setting up direct debits for utilities once you complete. Most Spanish banks now offer non-resident accounts that can be managed entirely through mobile apps for your convenience.

How do exchange rates affect my property purchase budget?

Currency fluctuations can shift your property budget by thousands of pounds in a single week. A 2% change in the GBP to EUR rate on a €300,000 property alters your cost by roughly £5,000. We recommend using a forward contract to lock in an exchange rate for up to 12 months. This is a crucial step on any saving for a second home in spain checklist for British buyers seeking financial certainty before they commit to a purchase.

Can I use rental income to pay off my Spanish mortgage?

You can use rental income to help pay off your mortgage, but Spanish banks won't include potential earnings in your initial mortgage application. They only consider your current guaranteed income from your home country. If you do rent your property out, remember that non-residents must pay tax on the income. EU residents pay 19%, whilst non-EU residents pay 24% as of early 2026. Professional rental management can help maximise these returns whilst you're away from the property.